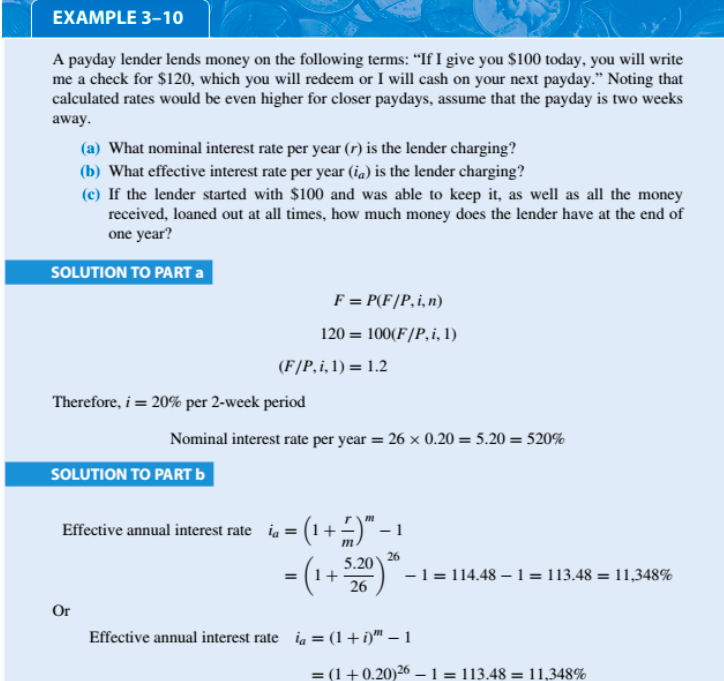

Ought i rating prequalified to own a mortgage?

It is better to get prequalified early in our home to get processes. When you find yourself just starting to consider buying or domestic hunting, prequalification is a straightforward process that will tell you how much you can afford that assist your set a spending budget.

Prequalification doesn’t make certain your own home loan acceptance. However it is a helpful tool when you’re simply starting due to the fact property visitors. And you will, because techniques try pared-off, you might usually rating prequalified easily and quickly on line.

What exactly is financial prequalification?

Prequalification is actually a primary step-in our home to buy procedure that can help you learn your financial budget and home loan selection. To obtain prequalified, you generally connect with a loan provider, respond to a couple of questions concerning your finances, and you may receive an offer of your own interest rate and loan amount you might be eligible for. Thus giving you an authentic cover home hunting.

Prequalification differs from preapproval as you don’t have to offer one data or experience a cards checkpared in order to preapproval, home loan prequalification was an easier and you will faster processes – however it is only a price of your budget rather than a great real approval.

How do i prequalify to possess a mortgage?

The mortgage prequalification techniques is relatively simple and quick. Online pre-certification forms tend to ask questions about your revenue, the amount of the deposit, and your established expense.

The financial institution can also run a mellow borrowing query observe details about your credit history and you may credit score. A smooth inquiry does not affect your ranking.

According to the suggestions you bring therefore the outcome of this query, the bank decides extent you may be able to acquire.

Prequalifications try short, so it’s not unusual to get a response within seconds. The lender will likely matter a prequalification page. This page is sold with the estimated amount borrowed and sometimes an estimated interest rate.

Recall, the loan number and you can rate you might be cited are not guaranteed until your bring complete documents and you may glance at the lender’s underwriting techniques. The prequalified mortgage count is just an offer.

At the same time, such emails try not to carry normally lbs as home financing preapproval letter. After you have a specific possessions you want, you are going to need to rating preapproved to confirm you really can afford they prior to an offer.

Home loan prequalification against. preapproval

- Prequalification is a quote considering your stated financials, whereas preapproval requires you to definitely fill in economic files

- Prequalification generally does not cover credit check Colorado installment loans and will not impression your own borrowing from the bank get, whereas preapproval needs a challenging credit query and you rating usually bring a little hit

Tips to acquire preapproved compared to. prequalified

Home financing preapproval requires a into the-breadth look at your finances than just when you get prequalified. The lending company have a tendency to gather help documentation prior to providing an endorsement.

- Salary stubs the past 1 month

- W-2s otherwise 1099s over the past a couple of years

- Tax returns regarding the prior 2 years

- Informative data on any types of earnings

- Checking account statements on early in the day sixty to help you 90 days

- Local rental background

- Photos ID

The lender must check if your revenue try uniform and you will secure and that you have sufficient cash spared for your down-payment and closing costs.

A home loan preapproval along with comes to a close look at the borrowing from the bank account. The lender not only considers your credit score but also your own previous credit rating. They lookup particularly at your fee history as well as your current bills.

Preapproval enables you to make a deal

Due to the fact a home loan preapproval concerns a deeper breakdown of your finances, an excellent preapproval page offers more excess body fat than simply a good prequalification letter. In reality, you usually you prefer an effective preapproval before you could even build an give for the a property. Good prequalification letter would not work on it phase since your cash have to be confirmed.

That have an excellent preapproval, you likely will become approved towards latest loan – provided your pointers can be verified and nothing transform in advance of closing.

When to score pre-eligible for a home loan

This post is valuable to own believe motives. You have an idea of just how much to keep for the downpayment and you will settlement costs, and you may know very well what can be expected with regard to home financing fee.

So if you’re refuted a prequalification, you could potentially take steps to change your debts before buying. This might are expenses your own expense timely, saving more income, settling obligations, and you may repairing errors in your credit file.

When you should get pre-accepted to have home financing

If you are looking absolutely at the home and ready to start making even offers, it’s time to score preapproved. The preapproval procedure commonly be sure you really can afford the house, and your preapproval page suggests owner and you may seller’s representative you may be capable to build a deal.

If you wish to circulate quickly, be sure to have the ability to debt documentation available to you when you make an application for preapproval. The new reduced you could render help documents on financial, quicker their preapproval tend to move (plus the at some point you can make a deal).

Home loan prequalification FAQ

Home loan prequalification could possibly get encompass a softer borrowing query. A softer inquiry isn’t really a formal credit comment, so it cannot impression your credit rating. Nevertheless helps the lending company gauge creditworthiness and determine exactly how much you might afford.

Specific mortgage brokers possess on the internet prequalification models. You could begin this new prequalification techniques of the finishing this form and you may bringing basic facts about your finances. This consists of factual statements about income and you will assets. Prequalification forms vary from bank so you’re able to lender. According to the lender, the proper execution you will consult factual statements about your credit rating and you can month-to-month loans payments.

Prequalification was a young step-in the borrowed funds process. It makes sense whenever you are preparing to purchase a property but you’re not yet , prepared to submit an offer. When you find yourself positively domestic hunting, a preapproval surpasses an excellent prequalification.

A great prequalification isn’t home financing approval. They simply quotes your probability of being approved. Prequalifications depend on self-said suggestions. For this reason, the lender doesn’t be sure your revenue, work, or possessions, nor can it over a proper writeup on your borrowing. To find a mortgage approval, you’ll need to render their lender that have help documentation and you may wait to possess an extensive borrowing from the bank research.

If you are prequalified and you’re willing to go-ahead with a home loan loan, the next thing is to do a formal mortgage software. At exactly the same time, you can easily give your own bank having help documents. This may involve previous paycheck stubs and you may W-2s, tax returns in the early in the day a couple of years, bank account statements, and you may a photo ID. The financial have a tendency to carefully remark your credit history and look particularly at your commission history and most recent financial obligation load.